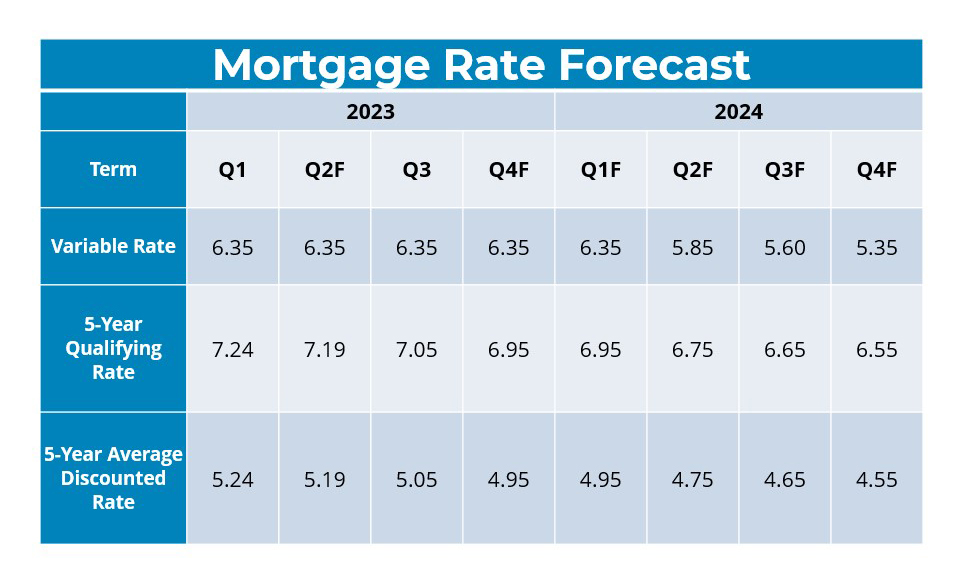

BCREA released it’s latest Mortgage Rate Forecast for 2023. To view the March 2023 Mortgage Rate Forecast PDF, click here.

Highlights:

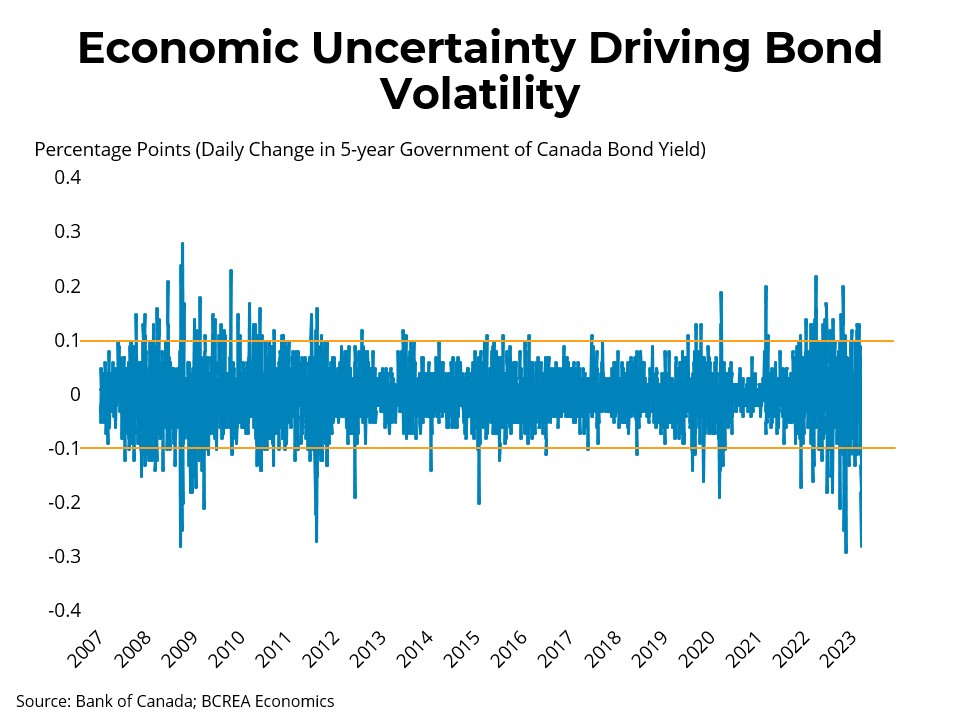

Economic uncertainty driving substantial volatility in Canadian bond markets.

Is the Canadian economy just slowing or something worse?

Inflation trending the right direction, will that be enough to keep the Bank of Canada on hold?

Click here to visit to BCREA’s website. To view other statistics for the Kamloops and BC real estate market click here.

If you want to be kept informed on Kamloops Real Estate, News and more visit our Facebook Page.

To search for Kamloops real estate and homes for sale click here.

“Copyright British Columbia Real Estate Association. Reprinted with permission.” BCREA makes no guarantees as to the accuracy or completeness of this information.

BCREA released it’s latest mortgage rate outlook. Read below and link to full report is included below.

The average Canadian 5-year fixed rate has fallen to under 2 per cent, the result of a rapid and overwhelming policy response from the Bank of Canada to the COVID-19 pandemic. The Bank swiftly brought its overnight rate to its effective lower bound of 25 basis points and used the impressive scope of its balance sheet to counteract a nascent rise in credit spreads. Those measures, and those of its global counterparts, helped to forestall a potential repeat of the credit crisis that shocked the global economy over a decade ago.

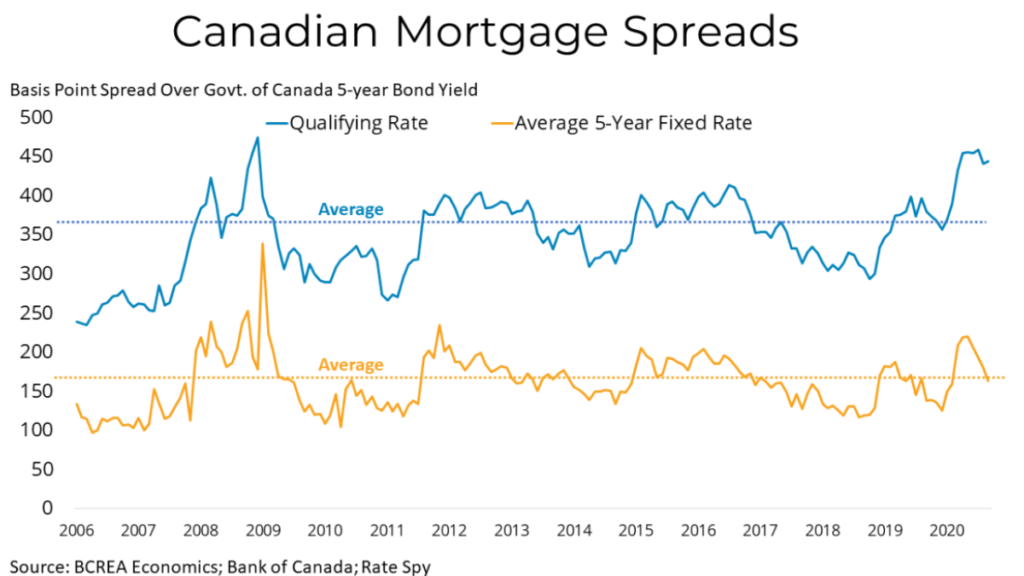

The Bank’s foray into quantitative easing (QE), or the purchasing of bonds across the yield curve of short-to-long term maturities, and an injection of liquidity into the mortgage market have resulted in record-low Canadian mortgage rates. The average 5-year fixed rate now sits below 2 per cent and is just 165 basis points over the 5-year government bond yield, essentially in line with the long-term average.

While the average 5-year rate has come down considerably, the qualifying rate remains stubbornly high at 4.79 per cent. That rate has become notoriously divorced from its underlying benchmark in recent years and now sits at a spread of close to 450 basis points over the 5-year bond yield, or about 100 basis points higher.

With the Bank of Canada eschewing negative interest rates and providing forward guidance that it has no plans to raise its policy rate until slack in the economy is absorbed, there is not much on the horizon that may move mortgage rates one way or the other. We expect a mild rise in rates as the Bank slows and eventually ends its QE, perhaps by the end of 2021. Studies show QE lowers long-term interest rates by 10-25 basis points, so we can anticipate a similar magnitude rise in 5-year rates when QE ends.

This article appeared on the Business News Network on January 14th, 2016 and was written by Fergal Smith of Reuters.

Bank of Canada interest rate cut speculation intensified on Tuesday as crude oil prices and the Canadian dollar both weakened to 12-year lows, with traders pricing in a full 25-basis-point easing by mid year.

The Canadian central bank cut rates twice in 2015 as an oil price shock drove the economy into recession in the first half of the year, but has been sidelined since July.

“People are calling for the Bank of Canada to cut rates at the next meeting,” said David Bradley, director of foreign exchange trading at Scotiabank.

The implied probability of a Bank of Canada rate cut at next week’s interest rate announcement has climbed from 22 percent after a speech by Governor Stephen Poloz last week to more than 30 percent, while the market has nearly fully discounted a rate cut in May.

The prospect of easing helped drive the yield on the Canadian government’s two-year bond to a four-month low.

Even so, “the market is underpricing the probability of a rate cut next week,” said Andrew Kelvin, senior rates strategist at TD Securities.

A Jan. 7 speech by Poloz had left investors doubtful he would cut Canada’s benchmark rate this month.

However, the central bank’s quarterly Business Outlook Survey has since found that business sentiment has deteriorated, while investment and hiring intentions have fallen to their lowest levels since 2009.

“It’s clearly going to be a very close call for the Bank of Canada given the financial turmoil we have seen,” said Kelvin.

U.S. crude oil prices have fallen an additional 8 percent this week, dipping below US$30 a barrel. Moreover, Western Canada Select, a blend produced by Canadian oil companies, trades at a greater than $14 discount to U.S. crude oil prices.

“We know falling oil prices have preceded both the last two cuts from the Bank (of Canada),” said Kelvin.

The central bank assumed a $45 price for U.S. crude oil prices when making its latest forecasts for the economy in October.

Speaking on Tuesday, Canadian Finance Minister Bill Morneau acknowledged that the public is concerned about the economy, but declined to indicate whether the government will stick to its budget deficit pledge or boost spending.

“We will be working in our budget to make sure that our initiatives help to grow the economy. We think the initiatives we already outlined are the appropriate initiatives to make a difference,” he said.

This article appeared on CBC.ca on the 29th of May 2015.

Canadians are showing a strong ability to manage their debts even as housing prices rise, with arrears on CMHC mortgages at a low 0.34 per cent for the first quarter of this year, according to new figures from the federal housing agency.

That means there were 9,572 Canada Mortgage and Housing Corp.-insured mortgages in arrears in the quarter, while it insures a total of 2.8 million mortgages. It had to pay just 588 claims.

The gross debt service ratio for Canadian homeowners – the percentage of housing costs to gross monthly income – sits at 26 per cent for the three months ended March 31.

That’s almost the same as in the first quarter of 2014, but up slightly from 25 per cent in 2013.

The ratios are highest in Alberta, British Columbia and Ontario, where housing prices have been rising rapidly. New homeowners in those provinces are also more likely to need a CMHC mortgage, which is necessary when buyers do not have a 20 per cent down payment.

However, a small proportion of CMHC-insured homeowners – 12.1 per cent – have a gross debt service ratio of more than 35 per cent, meaning more than a third of their monthly income goes to housing costs.

Another 21 per cent of CHMC-insured mortgage holders are juggling housing costs of 30 to 35 per cent of their gross income.

As housing costs rise, more than a quarter of the mortgages insured by CMHC are for over $400,000.

However, the average insured loan amount was $238,630.

In its annual report the federal agency predicts today’s low interest rates will continue to stimulate demand for housing.

It expects mortgage rates will not rise in Canada before the end of 2015.

The report comes after CEO Evan Siddall said CMHC’s share of the mortgage market had dropped from about 90 per cent of new mortgages to about half of new mortgages.

Ottawa had encouraged the agency to reduce exposure to mortgage defaults for the Canadian taxpayer, saying it wanted private insurers to take over the risk.

In its annual report, CMHC said it insured mortgages worth $543 billion in 2014, down 4.1 per cent from 2012, and below the legal limit of $600 billion.

This article appeared on the

This article appeared on the